New outbreaks, resilient growth in China, and increased stagflation in the United States and the European Union

According to international media, the virus outbreak in China signals an economic downturn, while the economies of the United States and the European Union have proven resilient. However, the data tells a different story about inflation, commodity crises, and misinformation wars in the West.

In the West, the international media has portrayed the Omicron disease outbreak in China as a vehicle for change that reflects the fall of the mainland. Will pressure on China then lead to the proposed influx of foreign multinationals, as some have suggested? The answer is no.

In 2021, the actual use of Chinese foreign direct investment amounted to more than 173 billion dollars, up 20.2 percent year on year in dollars. In the first two months of this year, foreign direct investment inflows rose to $37.9 billion, up 45.2 percent year on year.

Since early March, the Omicron outbreak has spread from Shanghai to other parts of China, including the provinces of Beijing, Guangdong and Hunan. So, how does China’s epidemiological performance compare to that of other countries?

Media attention versus reality

When China largely contained the Covid-19 outbreak in early 2020, the number of confirmed cases worldwide was around 3 million. Two years after the outbreak of the epidemic, the global figure was 516 million. There are more than 84 million confirmed cases in the United States alone, although the actual number is much higher. About 60 percent of Americans have contracted the virus, according to the US Centers for Disease Control and Prevention.

The failure of Washington and Brussels to contain the epidemic, along with insufficient international cooperation and stockpiling of vaccines in rich nations, has led to waves of new variables. The common denominator of these recent crises is the end of lockdowns, the opening up of economies, and the increase in international travel.

China is no exception, but it has a proven track record of rapid response and economic recovery.

Here are the facts: according to population size, the countries most affected are small and open trade economies such as Denmark (ranked 5) and the Netherlands (ranked 9); Major economies including France (14th), the United Kingdom (38th), and the United States (57th). The numbers are lower for Japan (129th) and developing countries such as the Philippines (146th) and India (150th). But China (223) ranks lower on the list. It has 152 cases per million people, compared to 249700 cases in the United States (Figure 1).

Figure 1 Cumulative confirmed COVID-19 cases per million people

Source: Johns Hopkins University CSSE Covid-19 Data, May 7, 2022.

In light of these facts, the argument that the scale of the Omicron outbreak in China exceeds the epidemiological devastation in the West is entirely false.

Destructive headwinds

The counterargument is that China occupies such a vital position in international value networks that severe turmoil in Shanghai, Beijing and Guangdong will have global repercussions. This is true, of course, but it also applies to foreign multinationals headquartered in the United States, European countries and Japan, which have suffered painful disruptions during epidemics.

It is clear that the gradual closure of China’s economic centers poses new challenges, including a slowing recovery in the automotive sector and increasing headwinds in the electronics sector. The slowdown is already evident in the sharp drop in the March PMI, along with weak import growth.

The impact of tensions in the global supply chain is significant in China due to the country’s primary role in global supply and distribution. However, other economies will experience stronger headwinds over time. The US Federal Reserve recently raised interest rates by 0.50 percent, the largest increase in 22 years. As the BoE is likely to follow in the Fed’s footsteps, pressure will mount on the European Central Bank to launch its rate plan.

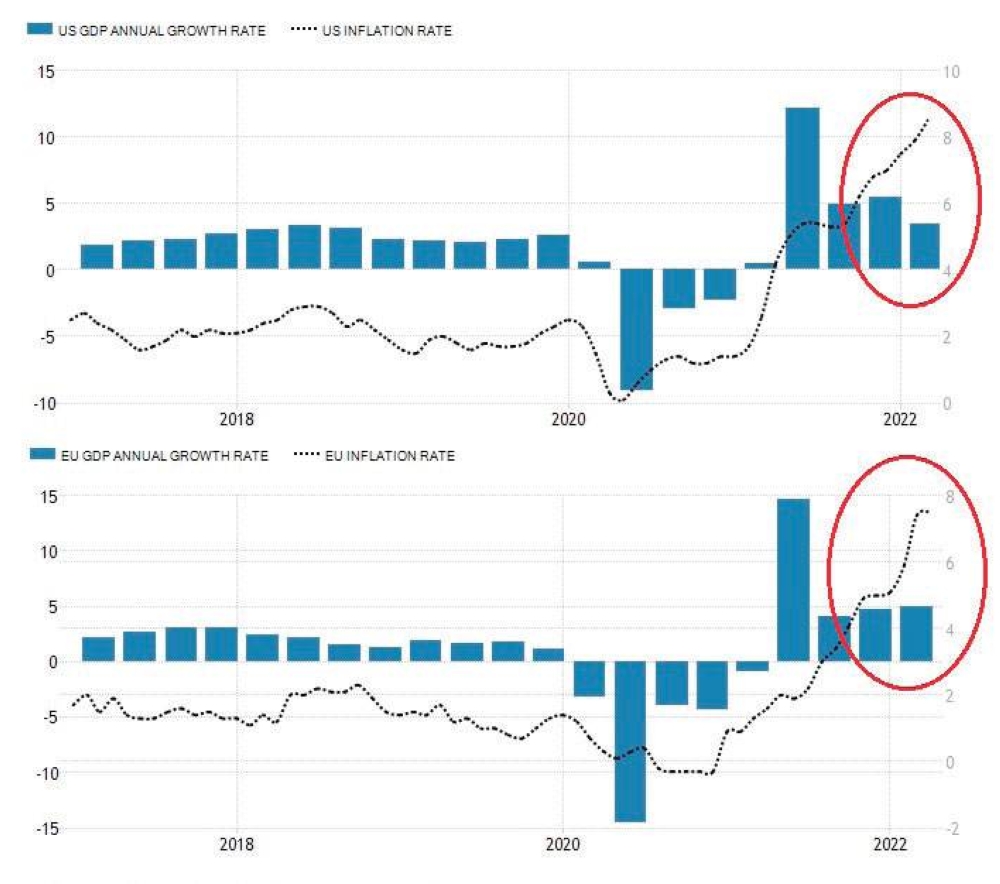

In the developed West, new headwinds will lower ratings in most major economies. In the US, the Biden administration, whose approval ratings have fallen from 53 to 38 percent, is seeing its highest inflation in 40 years, record trade deficits, weak growth and deflation in the first quarter. In the European Union, recession risks loom large. Inflation and rising interest rates are holding back growth in the United States and Europe (Figure 2).

Figure 2 – GDP growth and inflation: the United States and the Eurozone

Source: Trade Economics, Difference Group Ltd.

In Japan, growth forecasts were sharply revised downward. China is also facing new headwinds, but the premise — higher growth (4.8 percent in the first quarter, 1.5 percent lower inflation) — is more appropriate.

Unlike most advanced economies, China is trying to mitigate a sharp slowdown through moderate easing. Recently, the People’s Bank of China (PBoC) cut the required reserve ratio by 25 basis points, lower than the markets had expected. However, the People’s Bank of China is likely to implement more quantitative easing, including further reductions in program requirements.

The global headwind has just begun

Since March, the global economy has moved into the new, more dangerous status quo with rapidly mounting negative economic outcomes. As a result, global growth is expected to slow to 3.3% over the medium term, according to the International Monetary Fund. But this is a (very) benign scenario.

In addition to significant interest rate increases by the Federal Reserve and central banks of other rich economies, the coming shocks will be exacerbated by the ongoing crisis in Ukraine, ill-advised economic sanctions, and rearmament motives that could prolong and even widen the conflict. In addition, global prospects will be punished by energy and agricultural crises, a lack of proactive diplomacy, new viral strains, and devastating stagflation.

Without a broad reset of politics in the West, the current vicious circles will widen and deepen. As before, emerging economies will bear the bill.

Dr. Dan Steinbock is a global multipolar strategist and founder of The Teams Group. He has worked at the Institute of India, China and America (USA), the Shanghai Institutes of International Studies (China) and the European Union Center (Singapore). For more information see https://www.differencegroup.net.

“Travel enthusiast. Alcohol lover. Friendly entrepreneur. Coffeeaholic. Award-winning writer.”